Time really flies! It has been some thirty three years since I taught the course “Strategies for Investing in the Stock Market, Fundamental Analysis – Value Investing” at the University of Singapore, Extra Mural Studies Department (now known as NUS Extension). I was subsequently invited to teach Fundamental Analysis – Value Investing at the following institutions:

• The Singapore Stock Exchange (SGX) – A series of 7 lectures on Fundamental Analysis & Value Investing

• The Institute of Banking & Finance (IBF) – as a Continuing Education Program (CEP) on Fundamental Analysis & Value Investing

• The Securities Investors’ Association of Singapore (SIAS)

• Share Investor Pte Ltd.

The syllabus of the Value Investing Courses that I taught were distilled from the Value Investing principles of Benjamin Graham. David Dodd and Sidney Cottle and ideas from their investment classics – The Intelligent Investor and Security Analysis and also from my experience as Director of Research, Phillip Securities Research . Research Manager Morgan Grenfell Asia Pacific Securities (MGAPS) and as Vice President, Dealing, MGAPS. The Value Investing Course focussed on both a qualitative and quantitative analysis of companies relative to their peers in a given industry. The qualitative aspect focussed on the company’s durable competitive advantage , consumer monopoly, barriers to entry and its franchise value. The quantitative aspect of company valuation was a financial ratio based approach that was made up of 7 financial ratios( that I called the Basic Evaluative Ratios Test – BERT) namely dividend yield, price to earnings ratio, price to net asset value, reserves to issued capital, current ratio, return on equity and the debt equity ratio.It also included the Asset to Earnings Trade Off Multiplier used by Graham for conservative investors.

Although it was taught as part of my post graduate degree in finance, I was and have always been sceptical on using the Net Present Value (NPV) and Discounted Cash Flow (DCF)as applied to equity valuation because of the inaccuracies in forecasting cash flows and more so in determining the forecasted terminal value (which forms the bulk of value) and the assumed discount rate. Based on the positive feedback from the course participants and from the positive testimonials from the education commitees of the institutions that engaged me to teach, I knew that the contents of my courses was up to measure.

In 2001 , I read Professor Bruce Greenwald’s book titled “Value Investing from Graham to Buffet and beyond” and liked the approach presented. It was not only in 2007 that I realised that Prof Greenwald conducted a Value Investing Course as an Executive Education Program at Columbia University’s Graduate School of Business. Work, family and time constraints prevented me from attending the twice yearly program (note Prof Greenwald teaches in the June program while Professor Santos teaches the December program – please check it out at the Columbia Business School website).

Early this year in early April 2015,I decided to enrol for the Executive Education Program on Value Investing at The Columbia University Graduate School of Business . The program taught by Professor Bruce Greenwald was in late June 2015. I was accepted to the program in late May and in early June, I had to reread Prof Greenwald’s book “Value Investing from Graham to Buffet and Beyond” (actually my third reading) and to do pre-course homework on studying and analysing four public listed companies ( 1 company with listings on three exchanges). The pre-course preparation was quite exhausting but was quite a good learning experience.

Early this year in early April 2015,I decided to enrol for the Executive Education Program on Value Investing at The Columbia University Graduate School of Business . The program taught by Professor Bruce Greenwald was in late June 2015. I was accepted to the program in late May and in early June, I had to reread Prof Greenwald’s book “Value Investing from Graham to Buffet and Beyond” (actually my third reading) and to do pre-course homework on studying and analysing four public listed companies ( 1 company with listings on three exchanges). The pre-course preparation was quite exhausting but was quite a good learning experience.

In the morning of 21 June , I accompanied my twin daughters to their Brown Belt Grading in Aikido and the evening was spent celebrating Father’s Day with my four children and we revelled till just past midnight and I had two hours to pack for my flight from Changi Terminal One to Narita , Tokyo, Japan and then to John F Kennedy Airport , New York on 22 June and be at the Value Investing Program on the 23 June at Uris Hall, Columbia Business School, Columbia University. The 21 hour flight was a real pain. 7 hours to Narita, Japan , a stopover and another 14 hours to JFK Airport ,New York. I then realised that I had no sleep for the past 24 hours and tried to get some sleep on the flights by drinking wine followed by beers but that didn’t help. I arrived at JFK Airport slightly drunk and with a severe lack of sleep. I remember the first place I headed to was a Dunkin Doughnut stall for a much needed coffee and then took a 45 minute taxi ride to my hotel (NYLO) at the junction of Broadway and West 77 Street (close to Strawberry Fields at Central Park). I managed to get 8 hours of sleep before the course started on 23 June .

23 June 2015. I took the Number 1 train in the Subway from West 79 Street to West 116 Street (Columbia University Station) walked thru the West Walkway towards the University Library and to Uris Hall. As I walked past the University Library and the statue of the Scholar’s Lion , I could not help but feel the awe that I am at the birthplace of value investing. Here at Columbia University , the father of value investing – Benjamin Graham taught and instructed the the greats of value investing like Warren Buffet, Charlie Munger, Walter and Edwin Schloss, William Ruane, Micheal Price, Seth Klarman, Robert Klarman, Mario Gabelli, Glenn Greenberg and Robert Heilbrunn. Breakfast was at 8.15 am to 9.00am and the class started punctually at 9.00 am .

Professor Greenwald gave a brief introduction to the value investing program and went on to discuss various methods of valuation most notably the inherent weakness of the Net Present Value (NPV) / Discounted Cash Flow (DCF) Models. NPV and DCF models have an inherent weakness in that its inputs of future cash flows get more inaccurate the further it gets in the future and moreover the bulk of the forecasted value is in the terminal value that is in the future discounted to the present. How accurate can you get in the estimation of value that is ten years into the future? At this point, I could not help but recall that a few value investing experts who conduct courses on value investing in Singapore were using the DCF Model for their courses. If you think DCF is the best way to value companies, then you will have a problem.

Some salient considerations, search and valuation techniques covered by Professor Bruce Greenwald in the program are highlighted below.

• Not all value is measurable.

• Not all value is measurable by you (outside your circle of competence)

• Where do I have an advantage in valuation ? (what is my circle of competence)

• The three sources of value are : assets, earnings and growth. Values on assets are most reliable, values on earnings less reliable and values on growth being the least reliable. This point gave me most comfort because the value investing strategies that I taught were primarily asset based (in the Singapore context the focus was on property stocks) with earnings based valuations coming in a close second.

• Search strategies were highlighted . To be able to look for value opportunities , you must know where to look. Moreover valuation strategies must be appropriate to your search strategy. If you think Wells Fargo is overvalued , you may want to reconsider your valuation if your search strategy reveals that Warren Buffet is buying!

• The valuation technique using Asset Value and Earnings Power Value to pinpoint the qualitative aspect of the company concerned. This technique bridged the qualitative part of valuation with the quantitative aspect of valuation.

• The Asset Value(AV) is based on the reproduction value of the assets in the Balance Sheet. The Earnings Power Value (EPV) is Earnings multiplied by one divided by the Weighted Average Cost of Capital (WACC). Comparing AV with EPV we have three possibilities : 1. AV > EPV is a case where value is lost due to bad management or the company is in a industry downturn 2. AV = EPV is a situation where there is Free Entry Industry Balance (weak or no barriers to entry) 3. AV < EPV is a situation where the company has a superior management or competitive advantage – the question is will this situation be sustainable.

• Search Strategy – where to look for value opportunities and what is known as the Institutional Imperative.

Looking back at the Value Investing Program , I must say that I have learnt the following:

1. The traditional value investing techniques by Graham, Dodd and Cottle and as listed by Henry Oppenheimer that I used in my Value Investing and Fundamental Analysis courses are very relevant and useful in identifying value opportunities in stock investing.

2. The traditional Graham Dodd and Cottle Techniques that are primarily ratio based are now given another value investing dimension by considering reproduction costing of assets and of earnings by the Asset Value to Earnings Power Value perspective.

3. The Valuation Strategies are very much complimented by Prof Greenwald’s consideration of Search Strategies to identify Value Opportunities.

4. The least reliable source of value namely growth was dealt in detail with the conclusion that growth alone does not lead to value because growth comes at a cost. Growth without franchise destroys value. Growth contributes to value when there is franchise .

Looking back, I must say that the Value Investing Program at Columbia University’s Graduate School of Business was a fantastic opportunity for me to learn at the home of Value Investing and under the tutelage of Professor Bruce Greenwald. In addition to the traditional approaches to Value Investing pioneered by Graham, Dodd & Cottle et al , Professor Bruce Greenwald’s approach of using Asset Value and Earnings Power Value gives us a strategic dimension to modern day value investing by bridging the qualitative and quantitative aspects of company analysis.

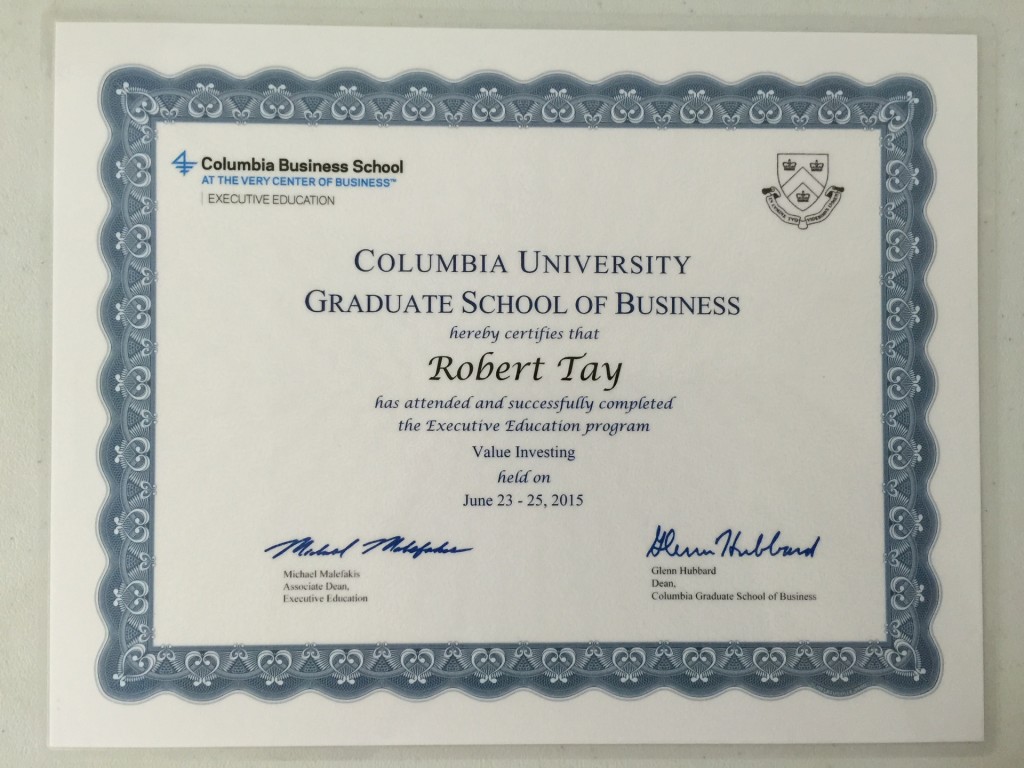

I am really grateful for the experience at the Value Investing Program at Columbia University’s Graduate School of Business and count it as an honor and a blessing in my journey as a value investor . I received a certificate of attendance and completion of the Executive Education Program on Value Investing.

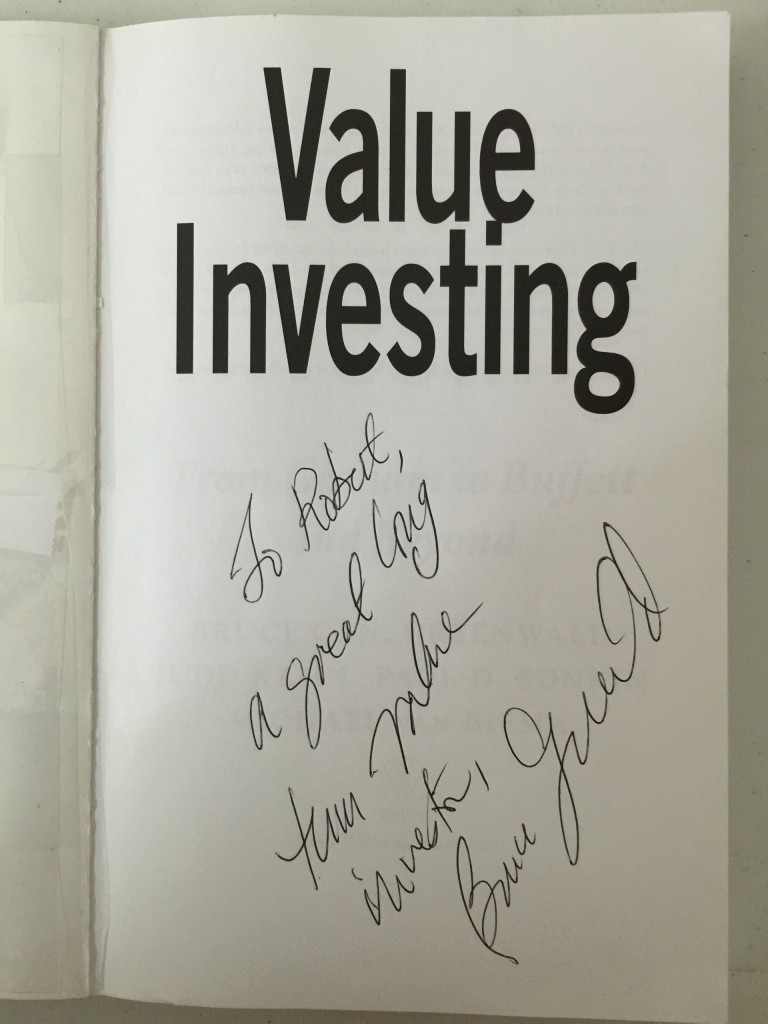

To top it all , Professor Bruce Greenwald autographed my copy of his book “Value Investing from Graham to Buffet and Beyond” and wrote “To Robert, a great long term value investor“.

I will be conducting an advanced program on Value Investing titled “ Fundamental Analysis – Advanced Value Investing” as a follow up to the present course that I teach titled “Fundamental Analysis- Basic Value Investing”. A prerequisite to attend the Advanced Value Investing Course is that you must have attended the Basic Value Investing Course.

If you are interested in the two courses, please email me at robert@investored.sg or call me at +65 97882803.